ROI Case File No.481 'The Morning Double-Entry Disappeared'

The Morning Double-Entry Disappeared

Chapter One: Days of Typing the Same Numbers Twice

"We're typing the same numbers twice. Once into the sales system, once into accounting."

Kenichi Watanabe, Sales Planning Director at TechSolutions, said this as he opened his laptop. The screen showed the current SFA system's input view, with the accounting system window open beside it.

"Every time an order closes, we travel between these two screens," Watanabe continued. "Customer name, amount, product code, delivery date—all of it goes into both. A mistake in one, and the month-end numbers stop matching."

"How many sales reps do you have?" I asked.

"Twenty-two," Watanabe answered. "Every one of them does the same thing. When an order report comes in, a sales rep spends an hour entering data into both systems, then accounting verifies it, and the accounting side reconciles the integrity again. Processing one order consumes nearly two hours across the organization."

"Is double-entry the only complaint about the current system?" Claude confirmed.

"No," Watanabe continued. "The UI is dated. Screen transitions are slow, search is weak. Customization quotes come back high and slow. There's no analytics, so we can't visualize sales and profit. Before monthly meetings, someone manually copies data into Excel to build the charts."

"What led you to consider replacement?" Gemini asked.

"The complaints have been there for three years," Watanabe answered. "But we couldn't figure out where to start. Change the SFA? Change the accounting system? Build integration between them? The axis for judgment was unclear. If we found the optimal system we could move, but optimal itself wasn't defined."

"You're searching for a product without having defined what optimal means," Claude said quietly. "That's why you couldn't move for three years."

Chapter Two: The Four Rotations OODA Demands

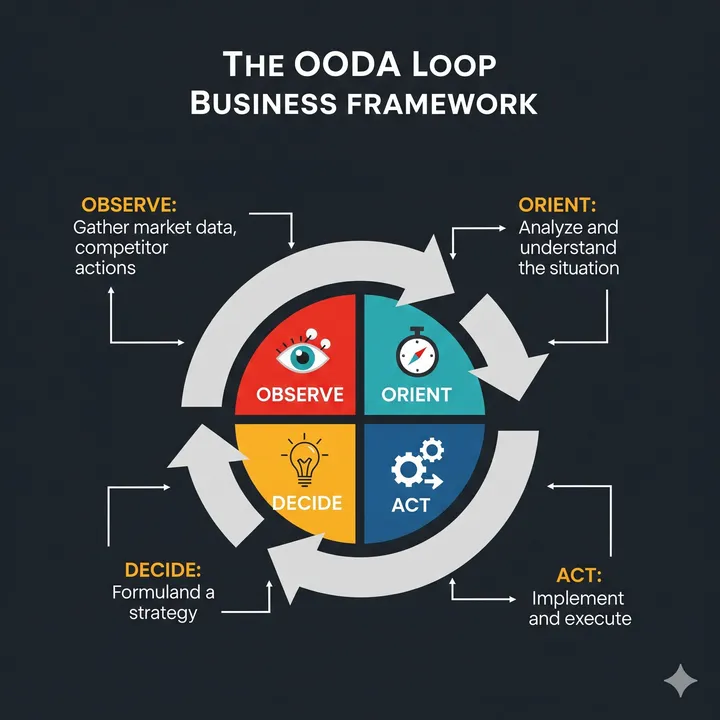

"This case needs OODA."

Claude wrote four letters on the whiteboard. O, O, D, A.

"OODA stands for Observe, Orient, Decide, Act—a decision-making framework that rotates these four stages at high speed," I explained. "PDCA starts from planning; OODA starts from observation. Observe what's happening in the field, orient it to your own situation, decide, and act—this four-stage rotation suits challenges where 'the optimal solution isn't a single fixed answer,' like system selection. Placing field observation ahead of comparison tables lets the judgment axis form naturally."

"Let's first measure the current cost," Gemini said, opening ROI Polygraph. The operational logs Watanabe had provided went in.

"The monthly double-entry cost is out," Gemini read. "Twenty-two sales reps averaging ten orders per month, thirty minutes of double-entry per order equals 110 hours monthly. At ¥4,000/hour that's ¥440,000 per month. Accounting-side integrity checks add 40 hours monthly at ¥3,500/hour, or ¥140,000. Monthly Excel processing for analytics adds 20 hours at ¥70,000. Manual workarounds for customization gaps add 25 hours at ¥100,000. Total: ¥750,000 monthly arising from structural inefficiency in the current SFA. Annualized: ¥9 million."

Watanabe stared at the figures. "Nine million a year. Larger than the initial cost of a new SFA."

"So, let's design with OODA," I continued.

[O—Observe: What's Happening on the Sales Floor]

"Start with field observation," Claude said. "Before product comparisons, have five sales reps shadowed for a day each to observe how they actually use the system. Where does time stall on which screen? Where do they click their tongue? That becomes the material for the next stage."

"What does observation reveal?" Watanabe asked.

"Unspoken dissatisfaction," Gemini answered. "The complaint 'the UI is dated' that you raised becomes quantifiable in the field—specific screen-transition counts, seconds per input field. Once numbers exist, they become evaluation axes for new SFA selection."

[O—Orient: What Requirements Fit TechSolutions]

"Bring the observation data into TechSolutions' context," I continued. "An SFA rated highly in the market may not fit your company. Industry, organization size, integration with existing systems, sales style—redefine requirements across these four axes."

"Accounting integration is an absolute requirement, right?" Watanabe confirmed.

"Separate absolute requirements from nice-to-haves," Claude answered. "Narrow absolutes to three: API integration with the accounting system, standard analytics dashboards, and usable UX without customization. Products that don't meet those three get dropped regardless of their overall reputation. Without narrowing, the comparison table swells and you can't move."

[D—Decide: Not by Comparison Table, but by Trial]

"In the Decide phase, catalog comparison isn't what matters," Gemini organized. "Narrow to three candidates and take a one-month trial with each. Five sales reps use them in daily work and compare against the numbers captured during observation. Input time, screen transitions, analytics-report build time—the product that improves these numbers most is the one selected."

"Doesn't that increase workload during trials?" Watanabe asked.

"It does," Claude answered. "That's why we limit it to five reps. A company-wide trial is too heavy. But the cost of choosing without trial and finding misfit in the field far exceeds the trial workload. The reason you couldn't move for three years is that you tried to decide without trying."

[A—Act: Phased Rollout to Earn the Field's Trust]

"In execution, avoid company-wide simultaneous switchover," I continued. "First month: the five selected reps only. Surface issues, fix them. Second month: one department. Third month: company-wide. Expanding in phases minimizes transition chaos."

"Let's run the investment plan through ROI Proposal Generator," Gemini suggested.

The introduction costs and savings from SFA replacement lined up.

- Initial cost: SFA introduction, accounting integration setup, data migration, and training totaling ¥3.2 million

- Monthly cost: New SFA license ¥180,000/month (¥40,000 more than current)

- Monthly savings: Double-entry elimination ¥440,000, integrity-check elimination ¥140,000, Excel processing elimination ¥70,000, manual workaround elimination ¥100,000, totaling ¥750,000

- Net monthly savings: ¥750,000 − ¥40,000 (increment) = ¥710,000

- Payback period: ¥3.2M ÷ ¥710,000 ≈ 4.5 months

"Payback within five months," Gemini summarized. "From year two onward, ¥8.5 million in annual net savings continues. Faster decision-making from improved analytics is an additional upside, not yet counted."

Watanabe said as he reviewed the numbers, "The decision I agonized over for three years turns out to be a five-month story in numerical form."

"Because you were searching for an optimal solution," I responded. "Starting from observation makes the optimal for your company visible in five months."

Chapter Three: A Culture of Trying and Then Deciding

"Let me organize the approach," I said at the whiteboard.

"Week one—shadow five sales reps. Record input times, screen transitions, points of irritation. Weeks two and three—redefine requirements and narrow to three candidate products. Weeks four to twelve—parallel trial of three products. Selected reps use each in daily work. Month three—compare trial data and decide. Month four—rollout begins with selected five only. Month five—one department. Month six—company-wide."

"Won't sales numbers drop during trials?" Watanabe confirmed.

"They might," Gemini answered. "But if any of the five produces results with the new system, other reps start wanting to use it voluntarily. Success from early adopters lowers resistance at rollout more effectively than mandate."

Watanabe closed his materials. "For three years I've been comparing catalogs. I wasn't comparing field conditions."

Chapter Four: The Morning Month-End Numbers Matched on Their Own

Seven months later, a report arrived from Watanabe.

The numbers from field observation exceeded his expectations. A single order entry averaged 32 minutes for a sales rep, 14 screen transitions, and the biggest frustration point was the search-results loading time. The product selected was the one that most improved all three indicators across the trials.

Three months after company-wide rollout, double-entry became structurally zero. Automatic data linkage from the new SFA to the accounting system went live, and month-end integrity checks became unnecessary. Watanabe wrote in his report, "Month-end numbers match without being made to match. The ordinary is now actually ordinary."

The analytics dashboards were complete with standard functionality. Excel processing before monthly meetings vanished, and meeting prep time shrank from three hours to thirty minutes. The sales director reported, "We now have more time for actual discussion in meetings."

Three of the five selected reps began fielding questions from other departments' sales teams. "It's being understood as a system they chose, not a system forced on them," Watanabe wrote.

It was a morning when no one was working a calculator at month-end.

"Searching for the optimal keeps you stuck for three years. Starting from observation gets you moving in five months. What OODA asks is not desk-bound comparison but what's happening in the field. The seconds a sales rep stalls on a screen, the screen transitions that provoke a tongue-click, the silent waiting for search results—when these become numbers, the definition of optimal sets itself. On the morning double-entry disappeared, the month-end numbers matched without being forced. A structure that didn't need to be matched was embedded in the system."

Related Files

Tools Used

- ROI Polygraph — Visualizing double-entry and integrity-check labor

- ROI Proposal Generator — SFA replacement payback simulation